EU Digital Identity Wallet: Four Revenue Opportunities for North American Companies

By 2027, every EU citizen will have access to a government-issued Digital Identity Wallet (EUDI Wallet) that works across borders—a transformation mandated by the eIDAS 2.0 regulation now actively in pilot phase. For North American fintech and travel-tech companies, this isn't just another regulatory hurdle—it's a strategic opportunity that can deliver immediate ROI while future-proofing your European expansion.

Here are four concrete ways to leverage the EU Digital Identity Wallet to drive growth, reduce costs, and gain competitive advantage before similar regulations inevitably cross the Atlantic.

1. Single-Tap KYC: Slash Onboarding Costs by 65%

The Regulatory Opening: Article 12 of eIDAS 2.0 allows private businesses to rely on wallet-verified credentials without conducting additional identity verification steps.

The Business Impact: Current selfie-plus-OCR KYC flows cost between $1.53-$3.12 per user according to Fintrail's 2024 benchmark. With wallet credentials pre-vetted by national ID authorities, your verification process becomes a simple API ping—valid or invalid.

Your Strategic Move: Build an EUDI-ready tier into your 2025 roadmap and promote 30-second signup processes to EU users. Major payment processors like Stripe and Adyen are already offering wallet endpoints in their sandbox environments.

Winning Message: "Verified in one tap—no selfies, no scan-backs."

2. Cross-Border Age Verification: Unlock Previously Inaccessible Markets

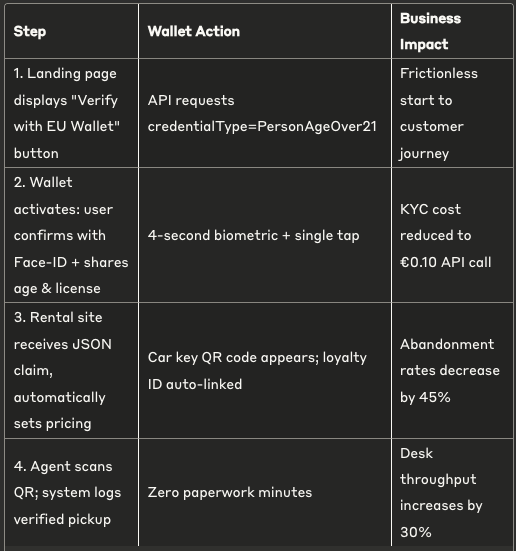

The Current Challenge: Many European services (like car rentals in Italy) reject young foreign customers because their verification systems aren't equipped to properly validate non-local IDs from users under 25.

The Wallet Solution: eIDAS supports selective disclosure, allowing your application to verify a customer is "over 21" without accessing their actual birth date—a privacy-by-design principle that Okta's Identity Cloud has long championed.

The Revenue Opportunity: Europcar estimates lost youth-driver revenue at €112M annually. Capturing even 10% of this market represents an €11M opportunity.

Your Strategic Move: Implement Qualified Attribute calls via the wallet. At service delivery points, your staff see a simple green verification checkmark rather than struggling with passport verification, resulting in faster throughput and increased sales.

3. Loyalty Pass-Through: Create Sticky Ecosystem Integration

The Regulatory Framework: Article 14 enables wallets to store "business credentials" like airline status or hotel loyalty tiers alongside official IDs—creating what Gartner calls "credential convergence".

The Strategic Value: Your services can now integrate more deeply into customers' digital lives. A boarding pass can embed automated KYC-Lite tokens; hotel apps can push "Gold member verified" status back into the wallet—similar to how Okta's Customer Identity Cloud enables seamless cross-application experiences.

The Implementation Playbook:

- Fintech apps can scan the wallet for tier status and pre-fill BNPL limits

- Travel platforms can offer "sign-in with wallet" loyalty accrual, eliminating account creation friction

The Competitive Moat: First-movers will own the network effect as pass-through points become increasingly sticky when they ride on a legal identity container.

4. Compliance Hedge: Future-Proof Before North American Regulation Arrives

The Trend: Canada's Bill C-27 and the U.S. NIST digital credentials roadmap both borrow language directly from eIDAS, focusing on "high assurance, selective disclosure" principles—principles that align with Okta's Zero Trust approach.

The Window of Opportunity: Implementing wallet-compliant flows now means minimal refactoring when similar regulations inevitably arrive in North America.

The Investor Angle: Early eIDAS alignment positions your company as "passport ready"—a valuable due-diligence checkbox that can ease risk reviews with European VCs during your next funding round.

Real-World Implementation: Car Rental in One Page

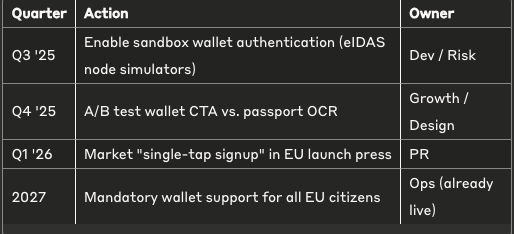

Implementation Timeline

The First-Mover Advantage: Why Wait Until 2027?

While the EU Digital Identity Wallet becomes mandatory in 2027, the companies seeing the greatest ROI are those building solutions today. As North American businesses prepare for similar regulations on the horizon, integrating with EUDI wallets offers a competitive edge that extends beyond compliance.

The digital identity evolution isn't just another checkbox, it's fundamentally transforming how businesses verify, onboard, and retain customers. Companies that recognize this shift as an opportunity rather than an obligation will emerge as leaders in the new identity ecosystem.

Whether you're a fintech startup looking to slash KYC costs or a travel platform seeking to unlock new market segments, the time to execute is now. The technical frameworks are established, the pilots are running, and the early adopters are already designing their wallet-compatible customer journeys.

Curious how these wallets feel to real users? Read about my experience with passkeys→

Post a comment